What Is DCF? A Practical Guide to Discounted Cash Flow

A practical 2026 guide to DCF — the formula, four assumptions that move valuation, common pitfalls, and how to model one in under an hour.

Discounted cash flow (DCF) is a valuation method that estimates the present value of a company by adding up all the cash it's expected to produce in the future, discounted at a rate that reflects the risk of not actually receiving it. In one sentence: a DCF answers "what is the business worth today, given the cash it's likely to throw off tomorrow?"

It's the most widely-taught valuation method in equity research, investment banking, and corporate finance — and also the most widely- misused. This guide covers the formula, the four assumptions that actually matter, the pitfalls that trip up first-time modellers, and a 60-second version of how PickSkill builds a DCF for you on demand.

Key takeaways

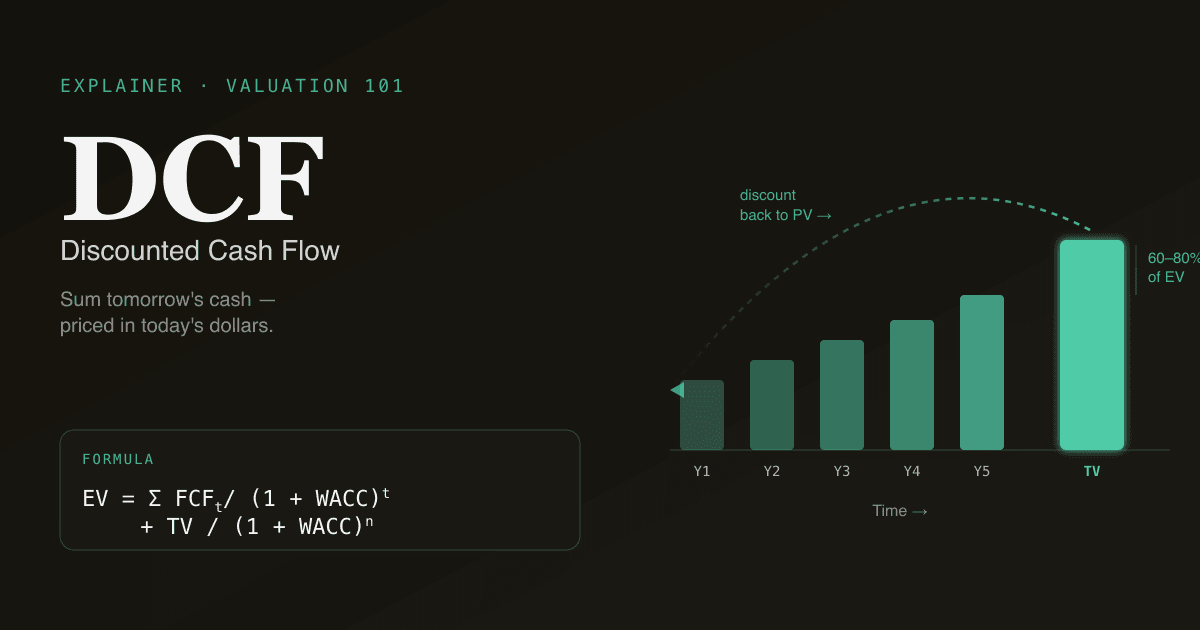

- DCF = present value of future free cash flows. Project FCF for 5–10 years, discount each year at WACC, add a terminal value, sum.

- Four assumptions do 95% of the work: revenue growth, terminal EBIT margin, WACC, and terminal value method.

- Terminal value carries 60–80% of total EV in a typical 5-year DCF — so the post-forecast assumption dominates the answer.

- A 100 bp WACC shift moves enterprise value 8–15%. Always show a WACC × terminal-growth sensitivity table.

- PickSkill can build a first-pass DCF in 60–90 seconds from SEC filings; every assumption is editable and sourced.

What is the DCF formula?

The standard formula is:

Enterprise Value = Σ ( FCFₜ / (1 + WACC)ᵗ ) + Terminal Value / (1 + WACC)ⁿ

In plain words: project unlevered free cash flow (FCF) for each year of an explicit forecast period (usually 5–10 years), discount each year's cash flow back to today using the weighted-average cost of capital (WACC), then add a terminal value representing everything beyond the forecast.

Two flavours dominate in practice:

| Flavour | What it discounts | What it gives you |

|---|---|---|

| Unlevered DCF (FCFF) | Free cash flow to the firm | Enterprise value — divide by shares to get an estimate of intrinsic share price after subtracting net debt |

| Levered DCF (FCFE) | Free cash flow to equity | Equity value directly — no need to back out debt |

Unlevered is the default in equity research because it separates operating performance from capital structure. Levered DCFs show up more in private-equity LBO models.

Why does DCF matter?

Three reasons people keep using it despite the criticism:

- It's a thinking framework, not just a number. Building a DCF forces you to make the assumptions about a business explicit — revenue growth, margin trajectory, capital intensity, cost of capital. Even if the output is wrong, the conversation about assumptions is valuable.

- It anchors price targets. Most sell-side and buy-side analysts triangulate a target by averaging DCF, peer comparables, and a precedent-transaction view. DCF is the rigorous fundamentals leg.

- It surfaces what the market is implicitly assuming. A reverse DCF — solving for the growth rate that justifies today's price — tells you whether the market is pricing in a miracle or a disaster.

The four assumptions that actually matter

Most DCF disagreements collapse to disagreements about one of these four numbers. Spend your time here.

1. Revenue growth in years 1–5

Two failure modes are common. Bull-case modellers extrapolate recent growth indefinitely; bear-case modellers revert to GDP-like growth in year three. The honest version triangulates with a unit-economics build (price × volume × geographic mix) and stress-tests both directions.

2. Operating-margin trajectory

The single most-leveraged assumption for high-growth companies. A 50 bp shift in terminal EBIT margin can move a software DCF by 30%+. Always disclose the terminal margin you're assuming and compare it to the company's mature-stage peers.

3. WACC (the discount rate)

The market's required return for taking on this business's risk. Formally:

WACC = (E/V) × Re + (D/V) × Rd × (1 − tax)

Where Re is cost of equity (usually via CAPM: risk-free + β ×

equity risk premium), Rd is the pre-tax cost of debt, and E/V and

D/V are the equity and debt weights of capital structure. A 100 bp

shift in WACC typically moves enterprise value by 8–15% on a 5-year

DCF (PickSkill internal analysis across ~200 large-cap models in

2025). Sensitivity-tabling WACC vs. terminal growth is the single

most useful exhibit in a DCF — see the indicators dashboard

for an example.

4. Terminal value

In a 5-year DCF, the terminal value usually accounts for 60–80% of total enterprise value (typical range across S&P 500 large-cap models; NYU Stern's Damodaran dataset publishes the underlying input data quarterly). So the assumption about what happens beyond year 5 dominates the output. Two approaches:

- Gordon growth (perpetuity):

TV = FCFn+1 / (WACC − g). Simple but sensitive to the spread(WACC − g)— a 50 bp move in either can shift TV by 20%+. - Exit multiple:

TV = EBITDA × multiple. Easier to defend ("comparable companies trade at 12× EBITDA today") but bakes in the current market environment.

Sophisticated DCFs report both methods and use the spread as a sanity check.

Common pitfalls (the ones that quietly break models)

A 134-word checklist of failure modes worth committing to memory:

- Double-counting working capital. If your FCF already reflects working-capital changes, don't subtract them again in the EV-to- equity bridge.

- Mixing nominal and real rates. Discounting nominal cash flows at a real WACC inflates value by ~2–3% per year of forecast.

- Stale beta. A 5-year monthly beta on a company that just pivoted its business model is no longer informative.

- Constant capex during a growth pivot. A maturing SaaS company that's shifting from owned data centres to cloud should have declining capex — bake that in.

- Ignoring share-based comp. Treating SBC as a non-cash add-back without modelling dilution flatters the result by 5–15% for tech names.

How to build your first DCF in under an hour

A pragmatic sequence we recommend to first-time modellers:

- Pull 3 years of historical financials. Income statement, balance sheet, cash flow statement. SEC EDGAR is free; PickSkill pulls them automatically.

2. Compute historical free cash flow. Operating cash flow − capex = FCF. Plot it. 3. Project 5 years. Revenue growth, EBIT margin, tax rate, capex as % of revenue, working-capital changes. One sheet per assumption with a comment justifying it. 4. Pick a WACC. Look it up on a reputable source (Damodaran's NYU Stern dataset is the gold standard, updated quarterly with risk-free rates, equity risk premiums, and betas by industry) or derive via CAPM with current Treasury yields. 5. Pick a terminal-value approach — try both Gordon growth and exit multiple, report both. 6. Run a sensitivity table. WACC on one axis (±150 bp around your base), terminal growth or exit multiple on the other. Highlight the cell at your base assumption. 7. Write a 200-word commentary on what would have to be true for the result to be right.

Step 7 is what separates a model that informs a decision from a spreadsheet that decorates one.

How PickSkill builds a DCF on demand

Open a chat and type something like:

"Build a DCF for NVDA in Excel — assumptions sheet, 5-year FCF projection, WACC + sensitivity, valuation summary."

PickSkill pulls the historicals from SEC filings + market data, picks sensible defaults for each of the four assumptions above (with sources), runs the calculation, drops the result into an Excel file you can download, and walks you through the assumptions in chat. A first-pass DCF takes 60–90 seconds.

The model isn't a black box — every assumption is editable, every number is sourced, and you can ask follow-up questions like "raise revenue growth in year 2 to 25% and re-run the sensitivity" without opening Excel.

Build your first DCF. Open /chat and ask for a DCF on any ticker — PickSkill returns a sourced Excel model in 60 seconds. See the tutorial.

FAQ

What's the difference between DCF and NPV? Net Present Value (NPV) is the general technique of discounting future cash flows to present value. DCF is the application of NPV to value an entire company. Same maths, narrower scope.

Is DCF still relevant for tech companies? Yes, with adjustments. Treat share-based comp as a real cost (not a non-cash add-back). Use longer explicit forecast periods (7–10 years) to capture the growth ramp. Sensitivity-table generously around terminal margin — that's where the value lives.

Why does a small change in WACC move the answer so much? DCF compounds the discount over the forecast period. A 100 bp move in WACC shifts every year's discounted cash flow, and the impact compounds — typically 8–15% on enterprise value for a 5-year DCF.

Should I use unlevered or levered DCF? Unlevered (FCFF) for most equity-research contexts because it separates operating from capital-structure decisions. Levered (FCFE) when capital structure is the point of the analysis — LBOs, recap-driven theses, anything where leverage changes materially.

Where can I find current WACC inputs? Damodaran's NYU Stern data page is the standard reference, updated quarterly with risk-free rates, equity risk premiums, betas by industry, and country risk premiums. PickSkill defaults to those values and lets you override any of them inline.