How to Read a 10-K in 30 Minutes — What Wall Street Actually Reads

What Wall Street actually reads in an SEC 10-K. The 4 Items (of 15) that carry signal, a 30-minute reading workflow, and the year-over-year diff technique.

A 10-K is the annual report every US-listed public company files with the SEC. It's the single most authoritative source of information about a business — written by management under legal liability, audited where it matters, and filed in a standard format. Read carefully, a 10-K answers almost every question that matters for an investment decision. Read carelessly, it's 150–300 pages of legal boilerplate that buries the signal in noise.

This guide is the 30-minute workflow professional analysts use: which four sections to read in depth, which 100+ pages you can skim or skip, and the questions to ask of each section. It assumes no prior accounting background — you don't need a finance degree, you need a map.

Key takeaways

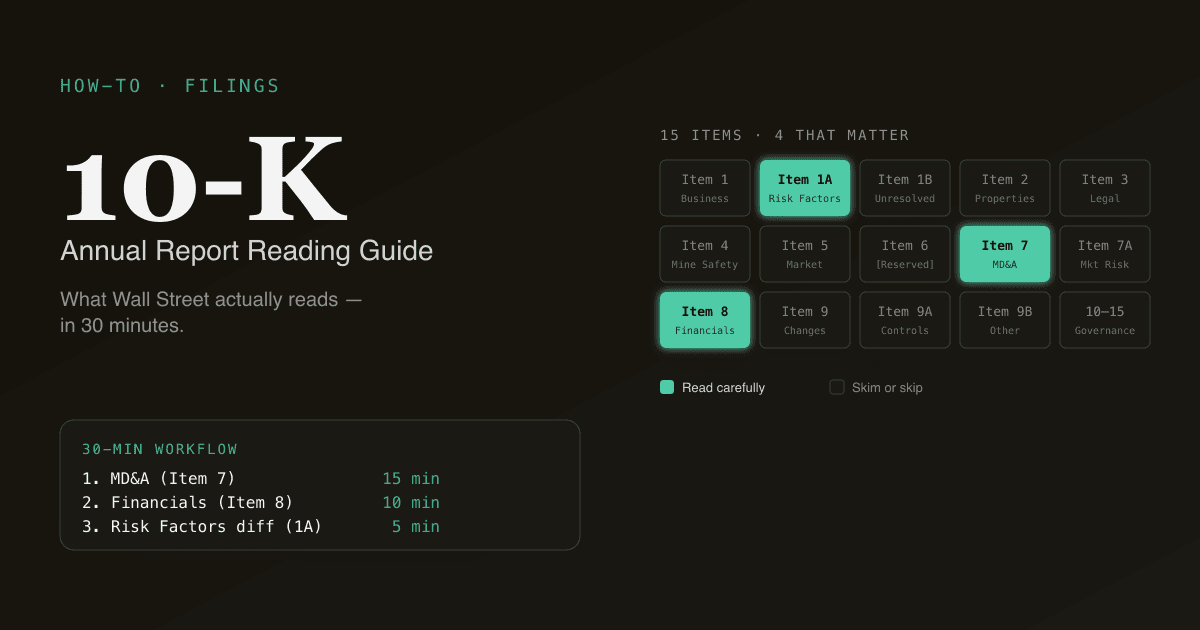

- A 10-K has 15 numbered Items across four parts. Four Items do 90% of the work; the rest is mostly boilerplate.

- Read in this order: Item 7 (MD&A) → Item 8 (Financials) → Item 1A (Risk Factors) → Footnotes you flagged. Skipping Item 1 (the business description) saves 20 minutes and loses very little signal.

- The cash flow statement is the most reliable section in the entire filing. Earnings can be reshaped within GAAP; cash either showed up or it didn't.

- Risk Factors used to be boilerplate — they aren't anymore. Since 2020, the SEC has pushed companies to surface specific risks; the genuinely new language in Item 1A is the most-read section by professional investors.

- PickSkill summarises a 10-K in ~60 seconds with the four sections that matter pulled out, the line items linked back to the source, and the year-over-year deltas pre-computed.

What is a 10-K?

A 10-K is the comprehensive annual report a US-listed public company files with the Securities and Exchange Commission within 60–90 days of its fiscal year end (depending on filer size). It contains audited financial statements, the management discussion that frames them, an explicit risk-factor disclosure, and a series of footnotes that explain the accounting choices behind the numbers.

It's filed publicly on EDGAR, the SEC's filing system, and is free to download. Every 10-K follows the same numbered structure — Items 1 through 15 across four Parts — which makes the document scannable once you know the map.

The 10-K's quarterly sibling is the 10-Q, filed within 40–45 days of each fiscal quarter end. A 10-Q is shorter (no audit, no full risk-factor refresh), and the workflow below works on it too — just expect less depth in the MD&A.

The four sections that actually matter

A 10-K has 15 Items. Read these four. Skim or skip the rest.

Item 7 — Management's Discussion and Analysis (MD&A)

What it is: Management's own narrative of the year, written in prose. Why revenue moved the way it did, what's driving the cost line, what they spent capex on, what they expect next.

Read time: 10–15 minutes. Worth every minute.

What to look for:

- Year-over-year revenue change broken down by segment or geography. Compare to last year's MD&A — are the same factors being cited?

- The "Liquidity and Capital Resources" subsection. This is where management talks about debt maturities, the cash position, and any financing needs. A company that suddenly devotes three paragraphs to liquidity that wasn't there last year is signalling stress.

- Non-GAAP measures the company emphasises (adjusted EBITDA, free cash flow, organic growth). Note which adjustments are being made; a growing list of "exclusions" is a yellow flag.

Item 8 — Financial Statements

What it is: The audited three statements — income statement, balance sheet, statement of cash flows — plus the footnotes that explain the line items.

Read time: 10 minutes for the statements, plus targeted footnote reading.

What to look for, in order of priority:

- Statement of Cash Flows. This is the least manipulable financial statement. The top of the operating-cash-flow section reconciles net income to cash from operations — every reconciling adjustment is a place where GAAP earnings differ from cash reality. (Free cash flow is

OCF − Capex; see What Is Free Cash Flow?.) - Income Statement. Read top-to-bottom looking for outsized changes in gross margin, operating margin, and any unusual one-off items in operating income.

- Balance Sheet. Focus on three lines: cash & equivalents (versus a year ago), total debt, and goodwill (large or growing goodwill = recent acquisitions; check whether they're earning their cost of capital).

Item 1A — Risk Factors

What it is: The risks management is required to disclose. Used to be 5–10 pages of stock language; since the SEC's 2020 modernisation rules, companies have been pushed to surface specific risks.

Read time: 5–8 minutes. The trick is reading diffs — what's new versus last year.

What to look for:

- New risk factors that weren't in last year's filing. These are almost always meaningful. A company doesn't add a new risk factor casually — adding language creates legal exposure, so the new language is there because legal counsel insisted.

- Risks tied to customer concentration (single customer >10% of revenue), supply chain dependency, regulatory change, or covenant compliance on debt.

- Risks the company addresses as a plural — "litigation matters" vs. "the lawsuit" — usually indicates an active dispute.

PickSkill auto-diffs Risk Factors against the prior year's filing and surfaces only the new or substantively changed language. That's the highest-signal chunk in a 10-K and the easiest one to miss when you read top-to-bottom.

Footnotes you flagged

What it is: 30–80 pages of detail behind every line item — revenue recognition policy, segment definitions, leases, tax positions, debt schedule, share-based compensation, commitments and contingencies.

Read time: Targeted — 5 minutes for the 1–3 footnotes you flagged while reading Items 7 and 8.

What to look for:

- Revenue recognition (usually Note 2). Subscription companies are required to detail their performance obligations and contract liabilities — these tell you about backlog and renewal risk.

- Debt schedule. Lists every facility, its rate, its maturity. Building a maturity wall chart from this table is the cleanest way to assess refinancing risk.

- Commitments and contingencies. Pending litigation, off-balance-sheet obligations, purchase commitments. The contingency you most want to find is the one management is being terse about.

- Income taxes. The reconciliation between statutory and effective rate. Big gaps = tax planning intensity; check whether the favourable items are sustainable.

The 30-minute workflow

A practical sequence:

- 2 min — Cover & contents. Confirm the period covered, the filer status (accelerated / non-accelerated affects deadlines), and locate Items 7, 8, and 1A.

- 15 min — Item 7 MD&A. Read top-to-bottom. Flag any footnote references you want to chase. Underline numbers you want to verify against Item 8.

- 10 min — Item 8 Financial Statements. Cash flow first, then income statement, then balance sheet. Pull the three numbers that matter: FCF, net debt, and YoY revenue growth by segment.

- 5 min — Item 1A Risk Factors diff. Compare to last year's 10-K and read only what's new or materially changed.

- 3 min — Targeted footnotes you flagged while reading.

Skip Item 1 (Business) unless this is your first time on the name — it's mostly stable boilerplate that repeats from year to year. Skip Items 9–15 unless you have a specific reason (executive comp, governance, etc.).

Common mistakes when reading 10-Ks

134 words worth memorising:

- Reading Item 1 top-to-bottom. Boilerplate. Skip unless first time on the name.

- Trusting non-GAAP without reconciling. Always find the GAAP-to-non-GAAP reconciliation table (usually right after MD&A or in an earnings release attached as Exhibit 99). The size of the bridge tells you how much management is adjusting away.

- Ignoring the Auditor's Report. A clean opinion is one paragraph long; anything more is a yellow flag (critical audit matters, qualified opinions, going-concern doubts).

- Reading only the current 10-K. The signal is in the diff against last year's. Risk Factors, MD&A language, and footnote disclosures only mean something against their prior-year baseline.

- Skipping the proxy. The proxy statement (DEF 14A) explains exec comp, board independence, and related-party transactions — material context the 10-K won't surface.

How PickSkill reads a 10-K for you

Open a chat and type:

"Summarise NVDA's most recent 10-K — give me MD&A highlights, the FCF, net debt, key Risk Factor changes vs. last year, and any footnotes I should look at."

PickSkill pulls the latest 10-K from SEC EDGAR, extracts Items 7, 8, and 1A, runs the Risk-Factor diff against the prior year's filing, computes FCF, WACC inputs (for a DCF if you want one), and surfaces a 90-second walk-through with each claim linked back to the page of the source filing. The whole thing takes ~60 seconds.

It's not a replacement for reading the filing yourself when the stakes are high. It's a way to know in advance which 4 sections to focus on and which 100+ pages to skim.

The 4 Items that actually carry signal

| Item # | Section | Why it matters |

|---|---|---|

| 1 | Business | Plain-English description of what the company does and how it makes money |

| 1A | Risk Factors | The legal-team list of things that could derail the thesis (year-over-year diff is gold) |

| 7 | MD&A (Management's Discussion) | Management's own explanation of the financials — read for what they don't say |

| 8 | Financial Statements + Notes | The numbers, plus the footnotes that explain accounting choices |

The other 11 Items are either boilerplate (executive bios, board structure, accountants engaged) or restatements of the financials in a different format. Skim, don't read.

FAQ

How is a 10-K different from a 10-Q? A 10-K is the annual filing — audited, comprehensive, with full Risk Factors and MD&A. A 10-Q is the quarterly filing — unaudited, shorter, and the MD&A is typically a delta against the prior quarter rather than a full narrative. Most professional analysts read 10-Qs for the cash flow statement update and the MD&A delta, and reserve deep reading for the 10-K.

When are 10-Ks filed? The deadline depends on the filer size: large accelerated filers (~$700M+ public float) file within 60 days of fiscal year-end; accelerated filers within 75 days; non-accelerated filers within 90 days. Most US large caps have December fiscal year-ends and file their 10-Ks in late February.

Where do I find a company's past 10-Ks? SEC EDGAR is the official, free archive. Search by company name or ticker. Past 10-Ks usually go back at least 20 years. PickSkill pulls directly from EDGAR — no third-party data middleman, so the numbers and language match the filing exactly.

Is the auditor's opinion always reliable? A clean ("unqualified") opinion means the auditor believes the statements fairly present the company's financial position in all material respects. It does not certify the business is healthy — only that the accounting is consistent with GAAP. Read the "Critical Audit Matters" subsection, introduced in 2019, for the items the auditor flagged as requiring extra judgement.

What's the fastest way to spot accounting red flags? Three signals from the cash flow statement: (1) widening gap between net income and operating cash flow, (2) operating cash flow that increasingly depends on working-capital releases (declining receivables, rising payables), (3) capex that has fallen sharply year-over-year. None of these is conclusive alone; combined they're worth investigating.