What Is the P/B Ratio? Price-to-Book Explained for Real Investors

P/B = price per share / book value per share. Formula, why P/B works for banks but not software, the trap of intangibles, and four pitfalls retail readers fall into.

The price-to-book ratio (P/B) compares a stock's market price to the accounting book value of its equity, expressed as a multiple. It is the third most-quoted valuation multiple after P/E and EV/EBITDA. It is also the most often misused — P/B works well for asset-heavy, balance-sheet-driven businesses (banks, insurance, real estate) and breaks down badly for software, services, and brand-driven businesses. Knowing where the line is matters more than knowing the formula.

Key takeaways

- Formula:

P/B = Price per share / Book Value per share. Book value per share = (Total Equity − Preferred Equity) / Shares Outstanding. - Below 1.0 = stock trades below accounting net worth. Usually means the market expects future losses, or assets are worth less than the balance sheet says.

- Where it works: banks, insurance, REITs, leasing, holding companies — businesses where balance sheet is the business.

- Where it fails: software, SaaS, consumer brands, biotechs — intangibles dominate, and accounting under-counts what the business is actually worth.

- The historical-mean comparison is more useful than the absolute level. A bank trading at 0.8× P/B when its 10-year average is 1.3× is signal; a bank trading at 0.8× P/B when 0.8× is its long-run average is noise.

How is P/B calculated?

Two equivalent formulations:

P/B = Market Cap / Book Value of Equity

P/B = Price per Share / Book Value per Share

Book value per share is computed from the balance sheet:

Book Value = Total Assets − Total Liabilities − Preferred Stock

Book Value per Share = Book Value / Diluted Shares Outstanding

The denominator (book value) is a historical-cost number that reflects what the company has cumulatively retained from earnings, plus any paid-in capital, minus any losses. For a business that has been profitable for decades, book value has compounded; for a heavily-acquired or heavily-restructured business, book value can be a long way from economic reality.

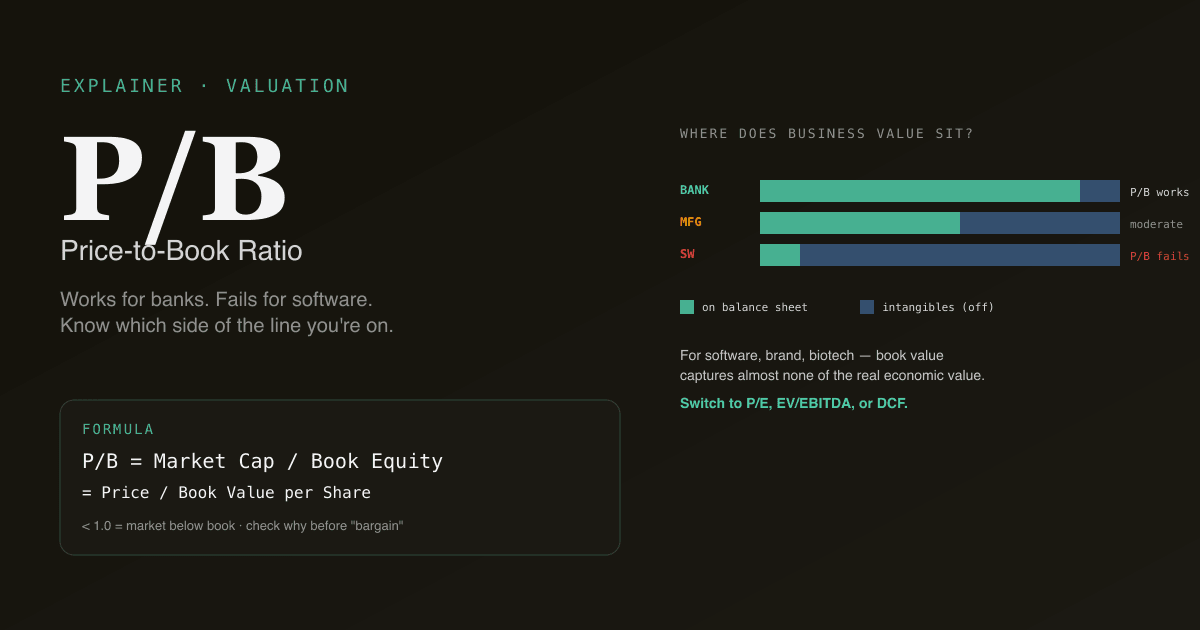

Why does P/B work for banks but not software?

The fundamental question is: how much of the business value sits on the balance sheet?

For a bank, the answer is almost all of it. A bank's primary assets are loans (recorded at amortized cost), securities (marked to market), and deposits (a liability). The business essentially is its balance sheet. P/B works because the multiple is comparing the market's view of the business to the literal accounting representation of the business.

For a software company, the answer is almost none of it. The valuable assets are: the engineering team (not on balance sheet), the brand (not on balance sheet unless acquired), the customer relationships (not on balance sheet unless acquired), and the IP (rarely capitalized). Accounting rules require these to be expensed when created, not capitalized. The balance sheet shows a small amount of capital, mostly cash and office equipment.

| Business type | Book value captures | P/B usefulness |

|---|---|---|

| Bank / insurance | Most of business value | High — primary valuation tool |

| REIT | Property at depreciated cost (often understated) | High — pair with NAV (net asset value) |

| Manufacturer | Plant + working capital | Moderate — useful with P/E for context |

| Software / SaaS | Negligible | Very low — use P/E, EV/Sales, EV/EBITDA |

| Consumer brand | Negligible | Very low — brand value is the asset |

| Biotech / pharma | Acquired IP, but pipeline is unrecorded | Very low — use pipeline NPV |

Applying P/B to a software company and concluding "it's at 25× P/B, it must be overvalued" misses the entire point of how the business creates value.

What does it mean when P/B is below 1?

A P/B below 1.0 means the market values the company at less than the accounting book value of its equity. Three possible interpretations:

- The market expects future losses. Cumulative future losses will erase part of book value. The market is right, the book value is wrong. Common in distressed banks during credit cycles.

- The accounting book value is inflated relative to economic reality. Goodwill from past acquisitions has not been impaired but should be. Inventory is obsolete. Loans will be written down. Common in restructuring situations.

- The market is wrong — there is value here. The "deep value" thesis. Famously profitable in financials post-2009, sometimes in commodities at cyclical lows. Rare and often a long wait.

A P/B below 1 in the financial sector is much more common than in other sectors. Banks routinely trade between 0.6× and 1.5× book through a cycle; this is not necessarily a bargain. A P/B below 1 in any other sector is usually a red flag worth investigating, not a buy signal worth chasing.

The intangibles trap

Modern accounting under-records intangibles. Examples of major business value that does not appear on the balance sheet:

- R&D is expensed, not capitalized. A pharma company that spent $30B on R&D over a decade shows zero of that on the balance sheet — but the IP and pipeline it produced may be worth $100B+.

- Brand is not on the balance sheet unless acquired. Coca-Cola's brand is worth tens of billions and shows up only as the goodwill from past acquisitions, not the value of the brand itself.

- Customer relationships in subscription businesses are valuable but mostly invisible until an acquirer assigns them a value.

- Team and culture never appear, despite being the most valuable asset in many businesses.

The P/B ratio for software, biotech, consumer-brand, and subscription businesses systematically overstates how expensive they look, because the denominator (book value) is structurally low relative to economic value. Sophisticated investors adjust by capitalizing R&D or by switching to EV/EBITDA or EV/Sales for these businesses.

Four pitfalls retail readers fall into

- Applying P/B universally. P/B is informative for ~25% of stocks (financials, REITs, asset-heavy industrials). For the other 75%, it is roughly meaningless. Match the multiple to the business model.

- Comparing P/B across industries. A bank at 1.5× P/B and a software company at 15× P/B are not the same kind of valuation — the multiples mean different things because what's in the denominator differs. Compare within industry only.

- Treating book value as static. Book value grows with retained earnings each quarter; it shrinks with buybacks below book and impairment charges. The right comparison is current price to current book value, not current price to last-year's book.

- Ignoring tangible book value for financials. Bank goodwill from past acquisitions sits on the balance sheet but evaporates in a crisis (most banks impair acquired goodwill during downturns). Sophisticated bank investors track tangible book value (book value minus goodwill and intangibles) as the more conservative reference.

How P/B fits in a multi-multiple framework

Use P/B alongside other multiples — never alone:

| Question | Best multiple |

|---|---|

| "Is this bank cheap?" | P/B + tangible P/B; cross-check with P/E |

| "Is this software company cheap?" | P/E + EV/Sales; ignore P/B |

| "Is this REIT cheap?" | P/NAV (net asset value); P/B as supporting reference |

| "Is this manufacturer cheap?" | P/E + EV/EBITDA + P/B for cycle context |

| "Is this consumer-brand company cheap?" | P/E + EV/EBITDA; P/B uninformative |

For absolute valuation, see What Is DCF? and DCF vs Comparable Company Analysis — multiples and DCF answer different questions and complement each other.

Run P/B analysis on your portfolio. In /chat, ask "for my financials holdings, show P/B and tangible P/B vs 10-year median, and flag any below 0.8× when the historical median is above 1.2×." PickSkill pulls the data and renders the comparison.

How P/B behaves differently across markets

| Market | Typical bank P/B range | Notes |

|---|---|---|

| US large-cap banks | 0.9× – 1.4× through cycle | Tangible P/B 1.0× – 1.5× often quoted alongside |

| EU banks | 0.5× – 1.0× through cycle | Structurally lower than US — partly persistent low ROE |

| HK / mainland banks | 0.5× – 1.0× recently | Compressed by margin pressure and regulatory headwinds |

| A-share state-owned banks | 0.4× – 0.7× | Persistent discount; market questions reported book value quality |

For A-shares, the P/B ratio is often quoted alongside dividend yield since SOE banks pay high yields, and the combination of low P/B + high yield is what attracts the value-trap-vs-value-opportunity debate.

Common follow-up prompts

- "Show me my financial-sector holdings' P/B vs 10-year median. Any structural cheapening?"

- "For [bank ticker], compare reported P/B to tangible P/B. What's the goodwill drag?"

- "Screen US regional banks with P/B below 1.0× AND ROE above 10% — the rare cheap-and-profitable combination."

- "What does Damodaran's industry data say about typical P/B for [sector]?"

Further reading

- Investopedia on P/B — comprehensive reference.

- Aswath Damodaran's quarterly P/B data by industry — the most-cited source for industry P/B benchmarks.

FAQ

Is a low P/B always a bargain? No — a low P/B often reflects accurate market pricing of an impaired business. In financials, persistent sub-1.0× P/B usually signals concerns about asset quality or future earnings power. The deep-value thesis (low P/B = bargain) works occasionally but requires identifying why the multiple is low and forming a view on whether the market is wrong. Most low P/B stocks deserve to be low P/B.

Why is P/B useless for tech companies? Tech companies create most of their value through R&D, brand, customer relationships, and team — none of which sit on the balance sheet under accounting rules. A tech company's book value reflects only cash, office equipment, and acquired goodwill, which is a tiny fraction of the underlying economic value. Applying P/B to a tech company is comparing market cap to an arbitrary accounting number that has little to do with business value.

P/B vs tangible P/B — which should I use? Tangible P/B (book value minus goodwill and intangibles) is the more conservative reference for financials, especially during stress periods. Goodwill from past acquisitions can be impaired in downturns, so tangible book is closer to the worst-case capital base. Use both: P/B for the headline, tangible P/B for the downside scenario.

Can P/B go negative? Yes — through aggressive buybacks at prices above book value, cumulative dividends exceeding retained earnings, or large impairment charges. When book value is negative, P/B becomes mathematically meaningless. For these businesses, switch to ROIC, earnings yield, or EV/EBITDA as the valuation reference. Apple, McDonald's, and Philip Morris have all flirted with negative book equity through buyback programs.

How does P/B compare to P/E? P/B uses balance-sheet capital as the denominator; P/E uses earnings power. P/E is more universally applicable because earnings are central to almost every business; P/B is more relevant only for businesses where the balance sheet captures most of the value. For most stocks, P/E is the more useful primary multiple. For financials, use both.